The One Big Beautiful Bill Act, signed into law on July 4, 2025, created a new car loan interest tax deduction that could save you hundreds to thousands of dollars when buying a new vehicle. For tax years 2025 through 2028, eligible buyers can deduct up to $10,000 in annual interest paid on qualifying auto loans, even if you take the standard deduction.

This rare tax benefit under Section 163(h)(4) of the Internal Revenue Code applies to new vehicles with final assembly in the United States, purchased for personal use. Unlike most auto-related tax breaks, this car loan interest deduction is available to both itemizers and non-itemizers, making it accessible to nearly every new car buyer who qualifies.

If you're shopping for a new vehicle in the Northwest Chicago suburbs, understanding this deduction could significantly impact your purchasing decision and long-term savings.

The auto loan interest deduction allows taxpayers to deduct interest paid on qualifying vehicle loans from their taxable income. This means you'll owe less in federal income taxes—potentially saving 10% to 32% of your annual interest payments, depending on your tax bracket.

Key Features:

This is one of the most significant vehicle-related tax benefits in recent history, designed to stimulate domestic auto sales and improve affordability for American car buyers.

Your vehicle must meet ALL of these criteria:

✓ New vehicle only

✓ U.S. final assembly

✓ Personal use

✗ Does NOT qualify:

Your auto loan must:

* Note: Refinancing a qualifying loan may remain eligible if secured by the original vehicle and within the refinanced amount.

The deduction begins to phase out based on Modified Adjusted Gross Income (MAGI):

Phase-out calculation:Your deduction is reduced by $200 for every $1,000 your MAGI exceeds the threshold.

Example: Single filer with $110,000 Modified Adjusted Gross Income (MAGI)

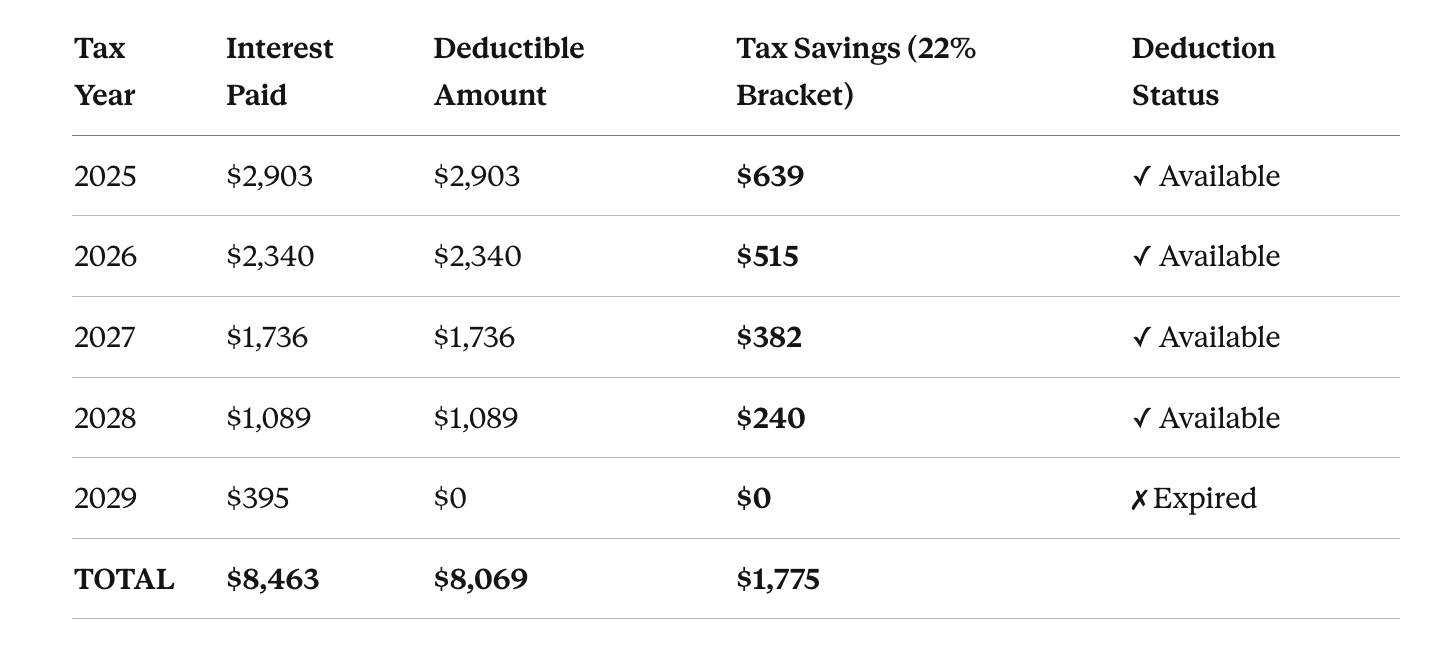

Let's look at a realistic scenario for an Illinois car buyer:

Key Insights:

Calculate your total car cost including financing with my free Out the Door Calculator tool.

Many Illinois car buyers wonder how state sales tax interacts with the federal car loan interest deduction. Here's what you need to know:

Illinois sales tax rates (2026):

Important: The car loan interest deduction is a federal income tax benefit. It does not reduce your Illinois sales tax, vehicle registration fees, or state income taxes. However, the federal tax savings can help offset these costs.

Example: $45,000 vehicle in Lake County

For a complete out-the-door price calculation including Illinois-specific fees and taxes, use my Free Out the Door Price Calculator.

Step 1: Obtain Your Interest Statement

Your lender must provide a statement showing total interest paid in 2025. For the 2025 tax year only, the IRS granted transitional relief—lenders can provide this through:

Step 2: Gather Your VIN

You must report your vehicle's VIN on your tax return. Find it on:

Step 3: Complete Schedule 1-A

The IRS created a new form specifically for this deduction. You'll need:

Step 4: File with Form 1040

Attach Schedule 1-A to your standard Form 1040. The deduction reduces your taxable income.

Starting with 2026 interest, lenders will provide a Form 1098-style document (similar to mortgage interest statements) showing:

Early in the year = More deductible interest

Since the deduction expires after 2028, buying earlier means more years of eligibility:

Recommendation: If you're planning a new vehicle purchase before 2029, buying sooner maximizes your total tax savings.

Shorter term = Higher monthly payment, but more concentrated interest

Consideration: A 48-60 month loan term balances monthly affordability with maximum deduction benefit.

Larger down payment = Less interest = Smaller deduction

This creates an interesting trade-off:

Example: $45,000 vehicle at 7%

Recommendation: Don't let the tax deduction drive you to borrow more than necessary. The interest you pay always exceeds the tax savings. You're still paying $0.78-$0.90 per dollar of deduction even after tax savings.

Understanding the car loan interest deduction is just one piece of the puzzle. When buying a new vehicle in the Northwest Chicago suburbs, you need someone who can:

I offer free consultations to help you:

Here are some useful links:

Common Questions About the Car Loan Interest Deduction

Yes! The deduction is retroactive to January 1, 2025. Any qualifying loan originated after December 31, 2024, is eligible. This means vehicles purchased throughout 2025 qualify for the full-year interest deduction when you file your 2025 taxes in early 2026.

If your MAGI exceeds $100,000 (single) or $200,000 (married filing jointly), you may still receive a partial deduction due to the phase-out structure. Only when your income reaches $150,000 (single) or $250,000 (married) is the deduction completely eliminated.

Yes—with limitations. If you purchased an eligible electric vehicle before September 30, 2025, you could have claimed both the EV tax credit (up to $7,500) and the car loan interest deduction. However, the EV tax credit expired on October 1, 2025, so vehicles purchased after that date only qualify for the interest deduction.

If you sell or trade the vehicle before the loan is paid off, you can no longer claim the deduction for interest paid after the vehicle is no longer secured by that loan.

Generally, no. If you refinance a qualifying loan and the new loan:

• Is secured by the same vehicle

• Does not exceed the refinanced amount

• Meets all other requirements

Then interest on the refinanced loan remains deductible.

If you use the vehicle partially for business, you can still claim the car loan interest deduction for the personal-use portion. However, you may get better tax benefits by deducting the business portion under business expense rules. Consult a tax professional to determine the optimal strategy.

Tax Advice Disclaimer:This article provides educational information about the car loan interest deduction under the One Big Beautiful Bill Act. It is not tax, legal, or financial advice. Tax laws are complex and individual circumstances vary significantly.

You should consult with a qualified tax professional, CPA, or tax attorney to:

V Knows Cars is a car buying consultation service, not a tax advisory service. We provide information to help you make informed decisions but cannot provide personalized tax advice.

Accuracy Disclaimer:This information is current as of January 2026 and based on IRS guidance available at that time. The IRS may issue additional regulations, clarifications, or updates that could affect eligibility, calculation methods, or reporting requirements. Tax laws may also change through future legislation.

Calculation Disclaimer:Examples provided use simplified scenarios for illustration. Actual interest paid, tax savings, and deduction amounts depend on:

Always verify calculations with your lender and tax preparer.

No Guarantee:The availability of this deduction, your eligibility, the amount you can deduct, and your actual tax savings may differ from examples shown. V Knows Cars makes no representations or warranties regarding your eligibility or potential savings.

Changes and Updates:The IRS continues to refine guidance on this new deduction. Visit IRS.gov for the most current information, including:

No pressure.

No obligation.

Just clarity.